FX Positioning: Dollar Short-Squeezing Emerges

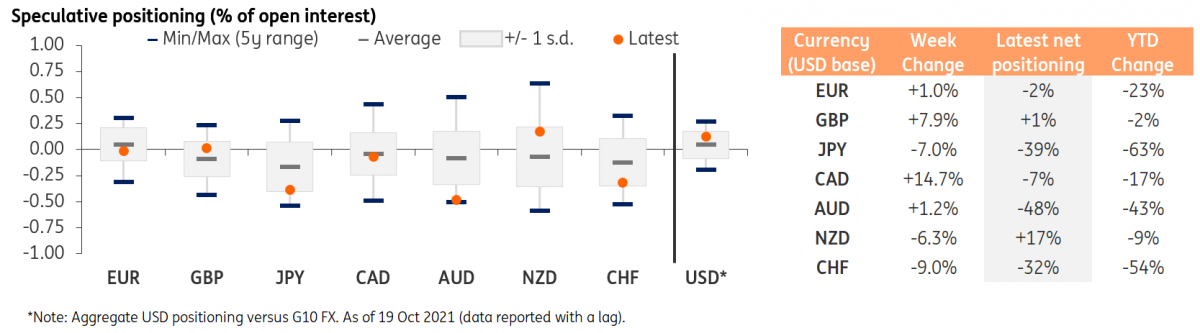

USD net longs shrink

CFTC data on FX positioning shows that, in the week ending 19 October, speculative investors decreased their net-long dollar exposure. The net aggregate dollar long positioning versus reported G10 currencies (i.e. G9 excluding NOK and SEK) fell from 14% to 12% in the past two weeks, after having risen quite steadily for the previous 17 weeks.

This is surely in line with movements in the FX spot market, as the dollar faced a downward correction in the past couple of weeks. We have been highlighting in our recent commentaries how we doubted that the dollar corrections was the start of a fresh USD bear trend, and instead observed how this could have been mostly due to some profit-taking on dollar positions, which was then exacerbated by a generalised improvement in global risk sentiment. CFTC data indeed show that the dollar started to face some squeezing of its long positions in the week ending 19 October, and we would not be surprised to see more evidence of this in next week’s COT report.

We remain of the view that the recent dollar weakness was transitory and that – as the Fed’s tapering and tightening cycles draw nearer – the dollar should re-join an appreciation trend soon.

Lots of wide swings in G10 positioning

As shown in the table above, the weekly changes in G10 FX positioning were quite significant. We are not too surprised to see a large swing in GBP and CHF positioning, as both currencies have shown a quite high volatility in their positioning gauges recently. Still, when it comes to GBP, a market that has moved to price in a November 15bp rate hike by the Bank of England likely contributed to push the pound’s net-positioning higher.

CFTC data also show a further drop in JPY net positioning, now at -39% of open interest. This is surely warranted by the recent rise in US Treasury yields, to which the yen holds a very strong negative correlation. JPY positioning is now at the bottom of its 1-standard-deviation band, but given the recent underperformance of US treasuries, we would not be surprised to see the yen’s net shorts build up again.

Among commodity currencies, the Canadian dollar saw a massive jump (worth nearly 15% of open interest) in net-positioning, with its net shorts now only worth 7% of open interest. This was due to a combination of rising energy prices (Canada is a big energy exporter), and a very encouraging economic data (especially on the labour-market side) that have both fuelled a hawkish re-pricing of Bank of Canada’s rate expectations, with markets now fully pricing in a rate hike in April 2022.

The Kiwi dollar, instead, saw its net longs squeezed in the week ending 19 October. This, however, appears to be a case of dislocation between positioning and market moves, as NZD was actually the best performing G10 currency in that week as inflation in New Zealand hit 4.9% and the case for faster RBNZ tightening obviously strengthened.

Source: ING