S&P 500 Index May Lead APAC Lower, Netflix Outlook Disappoints

S&P 500, Hang Seng Index, ASX 200 INDEX OUTLOOK:

- Dow Jones, S&P 500 and Nasdaq 100 indexes closed -0.89%, -1.10% and -1.34% respectively

- Netflix tumbled 19% during after-hour trade as its forward guidance disappointed investors

- China drafts rules to ease property curbs, sending Hong Kong stocks higher. Asia-Pacific markets open mixed

Netflix Earnings, Hong Kong Stock Rally, US Jobless Claims, Asia-Pacific at Open:

Wall Street equities fell for a third day as investors mulled mixed corporate earnings and the outlook for Fed tightening. Stocks gave up earlier gains and plunged in the final hour of trading, underscoring fragile sentiment. The Nasdaq 100 index has fallen more than 10% from its December high, entering into a technical correction. Investors are eyeing next Wednesday’s FOMC meeting for clues about the central bank’s roadmap for tightening. Policymakers may offer clues about the timing of the first rate hike and when it will consider to start balance sheet normalization.

Meanwhile, Netflix’s share price plummeted 19% during the after-hour trade as its forward outlook fell below market expectations. This happened even though the company has beaten on both top and bottom line estimates in Q4. Netflix said it expects to add 2.5 million subscribers during the first quarter of 2022, far below market expectations 6.93 million. It also marks a sharp decline from 8.28 million users added in Q4.

Hong Kong stocks soared on Thursday after news crossed the wires that China is drafting rules to give property developers more access to escrow funds. This will provide crucial help to developers to meet debt obligations, avoiding a serious cash crunch. The Hang Seng Index soared 3.42%, and the Hang Seng Tech Index surged 4.50% on Thursday. Both indices have breached above key resistance levels and may have reversed a prolonged downtrend. Developers, banks and technology shares were among the top gainers.

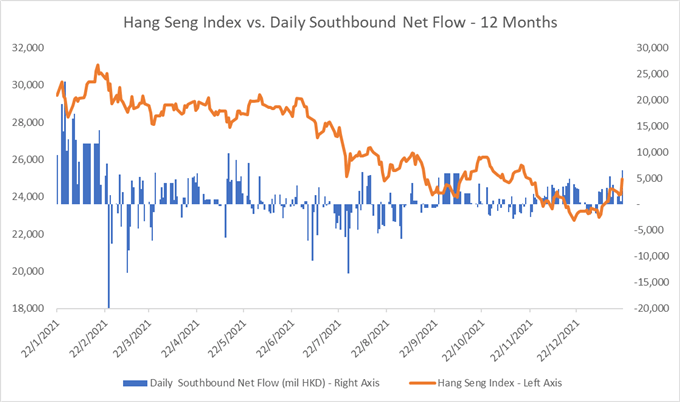

Chinese lenders have lowered borrowing costsfor a second straight month, in line with the PBOC’s move to cut 1-year MLF rate by 10bps earlier this week. This is another sign that the world’s second-largest economy is easing monetary policy to cushion an economic slowdown. Lower interest rates and the relaxation of property rules drive appetite towards Hong Kong shares, with the stock connection recording HK$6.54 billion of net Southbound inflows on Thursday, the highest seen since 31st August 2021.

Hang Seng Index vs. Southbound Net Inflow

Source: Bloomberg, DailyFX

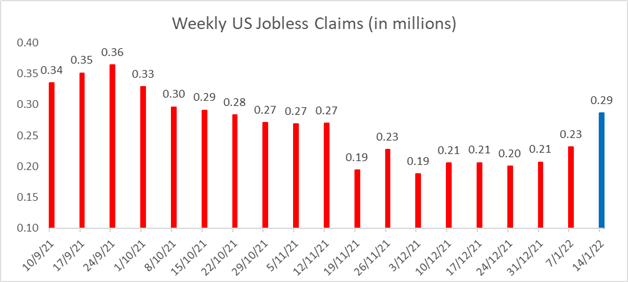

Meanwhile, weekly initial US jobless claims data came in at 286k, compared to a 220k estimate. This is also the highest reading observed in 14 weeks. The unemployment claims have been creeping higher in recent weeks, but the overall level is still substantially lower than the pandemic-era averages. With more companies citing rising wage pressure and challenges in hiring, this could be a short-term surge in unemployment claims.

US Weekly Jobless Claims

Source: Bloomberg, DailyFX

Read More: S&P 500 Index May Lead APAC Lower, Netflix Outlook Disappoints